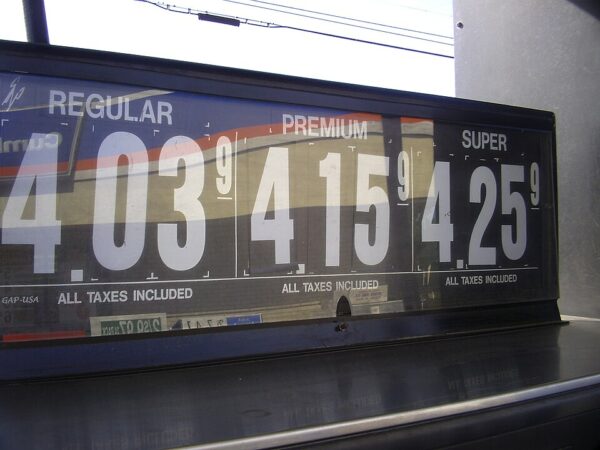

Americans are once again feeling the economic ripple effects of conflict abroad, as the national average price of gasoline climbed above $4 per gallon on Monday—marking a sharp increase tied directly to the ongoing war between the United States and Iran.

According to AAA, the average price for a gallon of regular gas now stands at $4.02, a level not seen since 2022 in the aftermath of Russia’s invasion of Ukraine. The sudden spike underscores how quickly instability overseas can translate into higher costs at home, particularly when critical energy routes are disrupted.

At the center of the surge is the closure of the Strait of Hormuz, a key global shipping lane through which roughly 20% of the world’s oil supply passes. With the route effectively shuttered amid the conflict, oil shipments have been restricted, tightening supply and sending shockwaves through international energy markets. As a result, crude oil prices have surged past $100 per barrel, driving up costs for consumers across the United States.

The impact, however, has not been evenly distributed. Prices vary significantly depending on location, with drivers on the West Coast bearing the brunt of the increase. In California, the average price for regular gasoline has reached $5.887 per gallon, placing an added strain on households already grappling with higher living costs. Meanwhile, states like Oklahoma have seen comparatively lower prices, with averages around $3.272 per gallon.

Overall, the national increase amounts to a roughly 35% jump, a steep climb that is likely to intensify concerns about the broader economic consequences of the conflict. While many Americans support a strong response to adversaries abroad, rising fuel prices serve as a reminder that such actions can carry real costs on the home front.

President Donald Trump has maintained that negotiations with Iran are ongoing, even as tensions remain high. He has repeatedly called for the immediate reopening of the Strait of Hormuz, framing it as a critical step toward stabilizing both the region and global markets.

In a post on Truth Social Monday, Trump stated that talks were progressing with what he described as a “new and more reasonable” regime. At the same time, he issued a stark warning, threatening to target Iran’s power plants, oil wells, and desalination facilities if a deal to reopen the strait is not reached immediately.

The dual messaging—expressing optimism about negotiations while also signaling the possibility of further escalation—reflects the high-stakes nature of the situation. On one hand, the administration appears to be pursuing a resolution that could ease pressure on global energy markets. On the other, the threat of additional strikes raises the possibility of prolonging the disruption.

Adding another layer of uncertainty, a report from The Wall Street Journal later indicated that Trump had privately acknowledged he might end the conflict without securing the reopening of the strait. Such a development could carry significant implications, both for the trajectory of the conflict and for energy markets already on edge.

For now, American drivers are left navigating the immediate consequences. As prices climb and uncertainty lingers, the situation highlights a familiar tension: the desire for decisive action abroad balanced against the economic realities felt at home.